US major ConocoPhillips' announcement last Friday that it will be pursuing the separation of its exploration and production (E&P) and refining and marketing (R&M) businesses into two separate publicly traded corporations via a tax-free spin-off R&M to COP shareholders does not surprise the Oilholic.

Rather, it is a sign of crude times. Oil majors are increasing turning their focus to the high risk, high reward E&P side of things rather than the R&M business where margins albeit recovering at the moment, continue to be abysmal. Most oil majors are divesting their refinery assets, and even BP would have done so, regardless of the Macondo tragedy forcing its hand towards divestment.

![]() ConocoPhillips’ decision should not be interpreted as a move away from R&M – nothing in the oil business is either that simple or linear. However, it certainly tells us where its priorities currently lie and how it feels the integrated model is not the best way forward. This is in line with industry trends as the Oilholic noted last November.

ConocoPhillips’ decision should not be interpreted as a move away from R&M – nothing in the oil business is either that simple or linear. However, it certainly tells us where its priorities currently lie and how it feels the integrated model is not the best way forward. This is in line with industry trends as the Oilholic noted last November.

Meanwhile, following the announcement, ratings agency Moody's says it may review ConocoPhillips' ratings for possible downgrade with approximately US$19.6 billion of rated debt being affected. This includes A1 senior unsecured and other long-term debt ratings of the parent company and its rated subsidiaries.

Tom Coleman, Moody's Senior Vice-President notes that the distribution to shareholders of the large R&M business could weaken the credit profile of ConocoPhillips and result in a downgrade of its A1 rating.

"Our review will focus on the company's capital structure following the spin-off, including the potential for debt reduction by ConocoPhillips, along with its financial policies and growth objectives going forward as a stand-alone E&P company," he concludes.

The wider market is waiting to get a clearer understanding of the oil major’s plans for debt reduction, capital structure and financial policies as an independent E&P. Continuing with corporate deals, BHP Billiton made a strategic swoop for Petrohawk Energy. The cash acquisition, also announced last Friday, to the tune of US$12.1 billion, will give it access to shale oil and gas assets across Texas and Louisiana. BHP’s latest move follows its earlier decision to buy Chesapeake Energy's Arkansas-based gas business for US$4.75 billion.

Meanwhile, figures released by Brazil’s Petrobras for the month of June indicate that the company’s domestic production rose 3.5% on an annualised basis. The results were boosted by the resumption of production on platforms that had been undergoing scheduled maintenance in the Campos Basin, and startup of a new well connected to platform Jubarte field's P-57 in the Espírito Santo section of the Campos Basin. The Extended Well Test (EWT) in the Campos Basin's Aruanã field also started up in late June.

Rather, it is a sign of crude times. Oil majors are increasing turning their focus to the high risk, high reward E&P side of things rather than the R&M business where margins albeit recovering at the moment, continue to be abysmal. Most oil majors are divesting their refinery assets, and even BP would have done so, regardless of the Macondo tragedy forcing its hand towards divestment.

ConocoPhillips’ decision should not be interpreted as a move away from R&M – nothing in the oil business is either that simple or linear. However, it certainly tells us where its priorities currently lie and how it feels the integrated model is not the best way forward. This is in line with industry trends as the Oilholic noted last November.

ConocoPhillips’ decision should not be interpreted as a move away from R&M – nothing in the oil business is either that simple or linear. However, it certainly tells us where its priorities currently lie and how it feels the integrated model is not the best way forward. This is in line with industry trends as the Oilholic noted last November. Meanwhile, following the announcement, ratings agency Moody's says it may review ConocoPhillips' ratings for possible downgrade with approximately US$19.6 billion of rated debt being affected. This includes A1 senior unsecured and other long-term debt ratings of the parent company and its rated subsidiaries.

Tom Coleman, Moody's Senior Vice-President notes that the distribution to shareholders of the large R&M business could weaken the credit profile of ConocoPhillips and result in a downgrade of its A1 rating.

"Our review will focus on the company's capital structure following the spin-off, including the potential for debt reduction by ConocoPhillips, along with its financial policies and growth objectives going forward as a stand-alone E&P company," he concludes.

The wider market is waiting to get a clearer understanding of the oil major’s plans for debt reduction, capital structure and financial policies as an independent E&P. Continuing with corporate deals, BHP Billiton made a strategic swoop for Petrohawk Energy. The cash acquisition, also announced last Friday, to the tune of US$12.1 billion, will give it access to shale oil and gas assets across Texas and Louisiana. BHP’s latest move follows its earlier decision to buy Chesapeake Energy's Arkansas-based gas business for US$4.75 billion.

Meanwhile, figures released by Brazil’s Petrobras for the month of June indicate that the company’s domestic production rose 3.5% on an annualised basis. The results were boosted by the resumption of production on platforms that had been undergoing scheduled maintenance in the Campos Basin, and startup of a new well connected to platform Jubarte field's P-57 in the Espírito Santo section of the Campos Basin. The Extended Well Test (EWT) in the Campos Basin's Aruanã field also started up in late June.

However, its international output was down 5.6% on an annualised basis due to operating issues and tax payments in Akpo, Nigeria. Petrobras' average oil and natural gas production (both domestic and overseas) amounted to 2,641,508 barrels of oil equivalent per day (boed), 2.13% up on the total figure for May 2011.

Finally, European woes are weighing on the crude markets. With the NYMEX August crude futures contract due to expire on Wednesday, intraday trading at one point, 1045 GMT to be precise, saw it down 0.31% or 33 cents at US$96.91 a barrel. Concurrently, the September ICE Brent futures contract was down 0.6%, 74 cents at US$116.44 a barrel.

© Gaurav Sharma 2011. Photo 1: COP Refinery & Oil Platform collage © ConocoPhillips

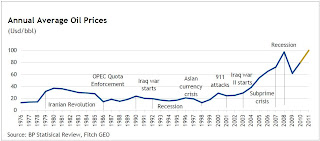

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)