It's the festive season alright and one to be particularly merry if you'd gone long on the price of black gold these past few weeks. The Brent forward month futures contract is back above US$110 per barrel.

Another (sigh!) breakout of hostilities in South Sudan, a very French strike at Total's refineries, positive US data and stunted movement at Libyan ports, have given the bulls plenty of fodder. It may be the merry season, but it's not the silly season and by that argument, the City traders cannot be blamed for reacting the way they have over the last fortnight. Let's face it – apart from the sudden escalation of events in South Sudan, the other three of the aforementioned events were in the brewing pot for a while. Only some pre-Christmas profit taking has prevented Brent from rising further.

Another (sigh!) breakout of hostilities in South Sudan, a very French strike at Total's refineries, positive US data and stunted movement at Libyan ports, have given the bulls plenty of fodder. It may be the merry season, but it's not the silly season and by that argument, the City traders cannot be blamed for reacting the way they have over the last fortnight. Let's face it – apart from the sudden escalation of events in South Sudan, the other three of the aforementioned events were in the brewing pot for a while. Only some pre-Christmas profit taking has prevented Brent from rising further.

Forget the traders, think of French motorists as three of Total's five refineries in the country are currently strike ridden. We are talking 339,000 barrels per day (bpd) at Gonfreville, 155,000 bpd at La Mede and another 119,000 bpd at Feyzin being offline for the moment – just in case you think the Oilholic is exaggerating a very French affair!

From a French affair, to a French forex analyst's thoughts – Société Générale's Sebastien Galy opines the Dutch disease is spreading. "Commodity boom of the last decade has left commodity producers with an overly expensive non-commodity sector and few of the emerging markets with a sticky inflation problem. Multiple central banks from the Reserve Bank of Australia, to Norges bank or the Bank of Canada have been busy trying to mitigate this problem by guiding down their currencies," he wrote in a note to clients.

Galy adds that the bearish Aussie dollar view was gaining traction, though the bearish Canadian dollar viewpoint hasn't got quite that many takers (yet!). One to watch out for in the New Year! In the wind down to year-end, Moody's and Fitch Ratings have taken some interesting 'crude' ratings actions over the last six weeks. Yours truly can't catalogue all, but here's a sample.

Recently, Moody's affirmed the A3 long-term issuer rating of Abu Dhabi National Energy Company (TAQA), the (P)A3 rating for TAQA's MYR3.5 billion sukuk programme, the (P)A3 for TAQA's $9 billion global medium-term note programme, the A3 rated debt instruments and the P-2 short-term issuer rating. Baseline Credit Assessment was downgraded to ba2 from ba1; with a stable outlook. It also upgraded the issuer rating of Rosneft International Holdings Limited (RIHL; formerly TNK-BP International) to Baa1 from Baa2.

Going the other way, it changed Anadarko's rating outlook to developing from positive. It followed the December 12 release of an interim memorandum of opinion by the US Bankruptcy Court, Southern District of New York regarding the Tronox litigation.

The agency also downgraded the foreign currency bond rating and global local currency rating of PDVSA to Caa1 from B2 and B1, respectively, and maintained a negative outlook on the ratings. Additionally, it downgraded CITGO Petroleum's corporate family tating to B1 from Ba2; its Probability of Default rating to B1-PD from Ba2-PD; and its senior secured ratings on term loans, notes and industrial revenue bonds to B1, LGD3-43% from Ba2, LGD3-41%.

Moving on to Fitch Ratings, given what's afoot in Libya, it revised the Italy-based Libya-exposed ENI's outlook to negative from stable and affirmed its long-term Issuer Default Rating and senior unsecured rating at 'A+'.

It also said delays to the production ramp-up at the Kashagan oil field in Kazakhstan were likely to hinder the performance of ENI's upstream strategy in 2014. Additionally, Fitch Ratings affirmed Shell's long-term Issuer Default Rating (IDR) at 'AA' with a stable outlook.

Moving away from ratings actions, BP's latest foray vindicates sentiments expressed by the Oilholic from Oman earlier this year. Last week, it signed a $16 billion deal with the Omanis to develop a shale gas project.

Oman's government, in its bid to ramp-up production, is widely thought to offer more action and generous terms to IOCs than they'd get anywhere else in the Middle East. By inking a 30-year gas production sharing and sales deal to develop the Khazzan tight gas project in central Oman, the oil major has landed a big one.

BP first won the concession in 2007. The much touted Block 61 sees a 60:40 stake split between BP and Oman Oil Company (E&P). The project aims to extract around 1 billion cubic feet (bcf) per day of gas. The first gas from the project is expected in late 2017 and BP is also hoping to pump around 25,000 bpd of light oil from the site.

The oil major's boss Bob Dudley, fresh from his Iraqi adventure, was on hand to note: "This enables BP to bring to Oman the experience it has built up in tight gas production over many decades."

Oman's total oil production, as of H1 2013, was around 944,200 bpd. As the country's ministers were cooing about the deal, the judiciary, with no sense of timing, put nine state officials and private sector executives on trial for charges of alleged taking or offering of bribes, in a widening onslaught on corruption in the sultanate's oil industry and related sectors.

Poor timing or not, Oman ought to be commended for trying to clean up its act. That's all for the moment folks! Have a Happy Christmas! Keep reading, keep it 'crude'!

To follow The Oilholic on Twitter click here.

To email: gaurav.sharma@oilholicssynonymous.com

© Gaurav Sharma 2013. Photo: Oil Rig © Cairn Energy.

© Gaurav Sharma 2013. Photo: Oil Rig © Cairn Energy.

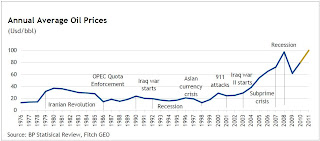

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)