To begin, while the end is nigh for the Gaddafi regime, a return to normalcy of oil production outflows will take months if not years as strategic energy infrastructure was damaged, changed hands several times or in some cases both. As a consequence production, which has fallen from 1.5 million barrels per day (bpd) in February to just under 60,000 bpd according to OPEC, cannot be pumped-up with the flick of a switch or some sort of an industrial adrenaline shot.

In a note to clients, analysts at Goldman Sachs maintain their forecast that Libya's oil production will average 250,000 bpd over 2012 if hostilities end as "it will be challenging to bring the shut-in production back online."

These sentiments are being echoed in Italy according to the Oilholic's, a country whose refineries stand to gain the most in the EU if (and when) Libyan production returns to pre-conflict levels. All Italy’s foreign ministry has said so far is that it expects contracts held by Italian companies in Libya to be respected by “whoever” takes over from Gaddafi.

Now, compound this with the fact that a post-Gaddafi Libya is uncharted geopolitical territory and you are likely to get a short term muddle and a medium term riddle. Saudi (sour) crude has indirectly helped offset the Libyan (sweet) shortfall. The Saudis are likely to respond to an uptick in Libyan production when we arrive at that juncture. As such the risk premium in a Libyan context is to the upside for at least another six months, unless there is more clarity and an abrupt end to hostilities.

Moving away from Libya, in a key deal announced last week, Russia’s Lukoil and USA’s Baker Hughes inked a contract on Aug 16th for joint works on 23 new wells at Iraq's promising West Qurna Phase 2 oil field. In a statement, Lukoil noted that drilling will begin in the fourth quarter of this year and that the projected scope of work will be completed “within two years.”

While tech-specs jargon regarding the five rigs Baker Hughes will use to drill the wells at a depth exceeding 4,000 meters was made available, the statement was conspicuously low on the cost of the contract. The key objective is to bring the production in the range of 145,000 to 150,000 bpd by 2013.

Meanwhile, Moody’s has raised the Baseline Credit Assessment (BCA) of Russian state behemoth Gazprom to 10 (on a scale of 1 to 21 and equivalent to its Baa3 rating) from 11. Concurrently, the ratings agency affirmed the company's issuer rating at Baa1 with a stable outlook on Aug 17th. The rating announcement does not affect Gazprom's assigned senior unsecured issuer and debt ratings given the already assumed high level of support it receives from the Kremlin.

Moody's de facto regards Gazprom as a government-related issuer (GRI). Thus, the company's ratings incorporate uplift from its BCA of 10 and take into account the agency's assessment of a high level of implied state support and dependence. In fact raising Gazprom's BCA primarily reflects the company's strengthened fundamental credit profile as well as proven resilience to the challenging global economic environment and negative developments on the European gas market in 2009-10.

"Gazprom has a consistent track record of strong operational and financial performance, which was particularly tested in 2009 - a year characterised by lower demand for gas globally and domestically, as well as a generally less favourable pricing environment for hydrocarbons," says Victoria Maisuradze, Senior Credit Officer and lead analyst for Gazprom at Moody's.

Rounding-off closer to home, UK Customs – the HMRC – raided a farm on Aug 17th in Banbridge, County Down in Northern Ireland, where some idiots had set-up a laundering plant with the capacity to produce more than two million litres of illicit diesel per year and evade around £1.5 million in excise duty. Nearly 6,000 litres of fuel was seized and arrests made; but with distillate prices where they are no wonder some take risks both with their lives, that of others and the environment. And finally, Brent and WTI are maintaining US$100 and US$80 plus levels respectively for the last seven days.

© Gaurav Sharma 2011. Photo: Veneco Oil Pumps © National Geographic. Table: Global commodities ETPs © Société Générale CIB/Bloomberg Aug 2011.

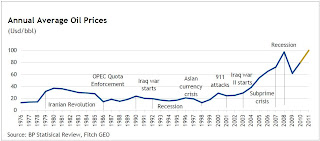

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)