In a surprising announcement here in Vienna, OPEC ministers decided not to change the cartel’s production quota contrary to market expectations. At the conclusion of the meeting, OPEC Secretary General Abdalla Salem el-Badri said the cartel will wait another three months at least before revisiting the subject.

In a surprising announcement here in Vienna, OPEC ministers decided not to change the cartel’s production quota contrary to market expectations. At the conclusion of the meeting, OPEC Secretary General Abdalla Salem el-Badri said the cartel will wait another three months at least before revisiting the subject.El-Badri also said the crude market was “not in any crisis” and that no extraordinary meeting had been planned. Instead, the ministers would meet as scheduled in December. However, he admitted that there was no consensus at the meeting table with some members in favour of a production hike while some even suggested a cut.

“Waiting (at least) another three months for a review was not to everyone’s liking but the environment around the table was cordial even though it was a difficult decision,” he said after the meeting. However, as expected, he did not reveal which member nations were for or against a decision to hold production at current levels.

El-Badri put OPEC's April production at about 29 million b/d and refused to answer many or rather any questions on Libya except for the conjecture that while Libyan production was not taking place, others can and will make up for the shortfall within and outside of OPEC.

The surprising stalemate at OPEC HQ has seen a near immediate impact on the market. ICE Brent crude oil futures rose to US$118.33, up US$1.55 or 1.3% while WTI futures rose US$1.30 to 100.61 up 1.3% less than 20 minutes after el-Badri spoke.

He added that the environment was cordial, but many suggested that it was anything but. The Saudis left the building in a huff with minister Ali al-Naimi describing it as the "worst meeting they have attended."

The analyst community is surprised but only mildly with many opining that the Saudis may well go it alone. Jason Schenker, President & Chief Economist of Prestige Economics says, “I think that what we have witnessed today is very similar to the group’s quota suspensions in the past. High volatility in the markets is clearly visible and there was no consensus at the meeting table about how to respond. At the end of the day, most OPEC member countries are going to react to what we have seen today as they see fit. Atop the list are the Saudis – the OPEC heavyweights - who will react as they always do and go it alone.”

Ehsan Ul-Haq, an analyst with KBC Energy Economics agrees with Jason. “Quite simply, if the Saudis want more oil on the market, they don’t need the Iranians, they don’t need the Venezuelans; they can and now probably will do it alone."

No wonder the new man at the table – the meeting’s President Mohammad Aliabadi of Iran spoke of a “nervous” two quarters for the oil market. The Oilholic felt this 159th ordinary meeting would be ‘extraordinary’ and so it has turned out to be. Venezuela, Iran and Algeria reportedly refused to raise production with a Gaddafi-leaning Libyan delegation backing their calls.

Meanwhile, the latest Statistical Review of World Energy published by BP earlier today with an impeccable sense of timing, noted that consumption of oil appreciated on an annualised basis at the highest rate seen since 2004. Christof Ruhl, BP group's chief economist, puts the latest growth rate at 3.1%.

According to BP, much of the increased demand for oil continued to come from China where consumption rose by over 10% or 860,000 b/d. The report also notes the continued decline of the North Sea with Norway, followed by the UK, topping the production dip charts. The take hike announced in the recent UK budget is not going to help stem the decline.

© Gaurav Sharma 2011. Photo: OPEC logo © Gaurav Sharma 2008

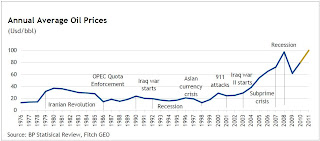

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)