The Eurozone sad show continues alternating from a Greek tragedy to an Italian fiasco and woes continue to hit market sentiment; contagion is now – not entirely unexpectedly – seen spreading to Italy with the country’s benchmark debt notes rates rising above the 7% mark at one point deemed ‘unsustainable’ by most economists. Inevitably, both crude benchmarks took a plastering in intraday trading earlier in the week with WTI plummeting below US$96 and Brent sliding below US$113. Let’s face it; the prospect of having to bailout Italy – the Eurozone’s third largest economy – is unpalatable.

The US EIA weekly report which indicated a draw of 1.37 million barrels of crude oil, against a forecast of a 400,000 build provided respite, and things have become calmer over the last 24 hours. Jack Pollard, analyst at Sucden Financial Research, noted on Thursday that crude prices gathered some modest upside momentum to recover some of Wednesday’s losses as equities pared losses and Italian debt yields come off their record highs.

“One important factor for crude remains the Iranian situation with Western diplomats adopting a decidedly more hard-line approach to their rhetoric. For example, the French Foreign Minister has said the country is prepared to implement ‘unprecedented sanctions’ on Iran whilst William Hague, British Foreign Secretary, has said ‘no option is off the table’. Should the geopolitical situation deteriorate, the potential for supply disruptions from OPEC’s second largest producer could provide some support to crude prices,” Pollard notes.

From a Brent standpoint, barring a massive deterioration of the Iranian scenario, the ICE Brent forward curve should flatten in the next few months, mainly down to incremental supply of light sweet crude from Libya, end of refinery maintenance periods in Europe and inventories not being tight.

In an investment note to clients, on October 20th, Société Générale CIB analyst Rémy Penin recommended selling the ICE Brent Jan-12 contract and simultaneously buying the Mar-12 contract with an indicative bid @ +US$1.5/barrel. (Stop-loss level: if spread between Jan-12 and Mar-12 contracts rises to +US$2.5/barrel. Take-profit level: if spread drops to 0.)

The Oilholic finds himself in agreement with Penin even though geopolitical risks starting with Iran, followed by perennial tensions in Nigeria, and production cuts in Iran and Yemen persist. But don’t they always? Many analysts, for instance at Commerzbank, said in notes to clients issued on Tuesday that the geopolitical climate justifies a certain risk premium in the crude price.

But Penin notes, rather dryly, if the Oilholic may add: “All these factors have always been like a Damocles sword over oil markets. And current disruptions in Nigeria, Yemen and Iraq are already factored in current prices. If tensions ease, the still strong backwardation should as well.”

Additionally, on November 1st, his colleagues across the pond noted that over the past 20 years, when the NYMEX WTI forward curve has flipped from contango into backwardation, it has provided a strong buy signal. Société Générale CIB, along with three others (and counting) City trading houses recommend buying WTI on dips, as the Oilholic is reliably informed, for the conjecture is not without basis.

There is a caveat though. Société Générale CIB veteran analyst Mike Wittner notes that it is important to take into account the fact that crude oil stocks at Cushing, Oklahoma, consist not only of sweet WTI-quality grades but also of sour grades. “Most market participants, including us, do not know the exact breakdown between sour and sweet crudes at Cushing, but the recent move into backwardation suggests that there is little sweet WTI-quality crude left,” he adds.

Société Générale CIB analysts believe market participants who are reluctant to go outright long WTI in the current highly uncertain macroeconomic environment may wish to consider using the WTI sweet spot signal to go long WTI against Brent. Any widening of the forward-month Brent-WTI spread towards US$20 represents a trading opportunity, as the spread should narrow to at least US$15 and possibly to as low as US$10 before year-end, on the apparent shortage of WTI and increasing supply of Atlantic Basin waterborne sweet crude.

© Gaurav Sharma 2011. Photo: Trans Alaska Pipeline © Michael S. Quinton / National Geographic

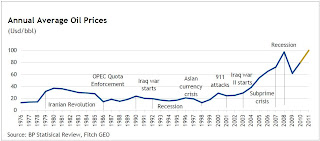

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

.jpg)