One has to hand it to ExxonMobil’s inimitable boss – Rex Tillerson – for successfully forging an Arctic tie-up with Rosneft so coveted by beleaguered rival BP. On August 30, beaming alongside Russian Prime Minister Vladimir Putin, Tillerson said the two firms will spend US$3.2 billion on deep sea exploration in the East Prinovozemelsky region of the Kara Sea. Russian portion of the Black Sea has also been thrown in the prospection pie for good measure as has the development of oil fields in Western Siberia.

One has to hand it to ExxonMobil’s inimitable boss – Rex Tillerson – for successfully forging an Arctic tie-up with Rosneft so coveted by beleaguered rival BP. On August 30, beaming alongside Russian Prime Minister Vladimir Putin, Tillerson said the two firms will spend US$3.2 billion on deep sea exploration in the East Prinovozemelsky region of the Kara Sea. Russian portion of the Black Sea has also been thrown in the prospection pie for good measure as has the development of oil fields in Western Siberia.The US oil giant described the said deal as among the most promising and least explored offshore areas globally “with high potential for liquids and gas.” If hearts at BP sank, so they should, as essentially the deal has components which it so coveted.

The Oilholic is pretty stumped too for harbouring the belief that BP's Arctic deal with Rosneft – originally agreed in January but scuppered by a legal challenge from Russian co-investors in BP's existing Russian joint venture TNK-BP – would be revived. It seems what BP could not manage, ExxonMobil did, and successfully fought off Shell in the process as well if the City rumour mill is to be believed. Some won, some lost, some got stumped but one looked like a moron or hypocrite or possibly both. That is none other than US Congressman Ed Markey, a Massachusetts Democrat on the House Natural Resources Committee.

Remember when BP first announced its proposed tie-up Rosneft back in January? At the time Markey quipped "BP once stood for British Petroleum. With this deal, it now stands for Bolshoi Petroleum." Bolshoi actually means “big” in Russian so it seems while Markey had right context for the slur, he ended up choosing the wrong word.

As the news of the Exxon-Rosneft tie-up emerged, Eben Burnham-Snyder, Markey's spokesman, told the Associated Press that the Congressman's office is looking into the Exxon-Rosneft deal. But he said the deal doesn't appear to involve the same ownership issues that were involved in the BP-Rosneft stock swap. Tut, tut, sir! Of course they don’t – after all this time it is an American firm that’s gone fishing.

As if with impeccable timing, barely a day after Exxon-Rosneft deal was inked, Russian Bailiffs raided the offices of BP in Moscow, seeking documents on its failed deal with Rosneft. According to RIA Novosti, the raid was conducted in line with a ruling by an arbitration court in the Siberian region of Tyumen, which is hearing a case over the Rosneft deal that collapsed in May.

Minority shareholders are claiming that TNK-BP suffered losses of US$3 billion as a result of the wrangling over the now failed BP-Rosneft joint venture. In a statement, BP confirmed that its Russian offices in Moscow were raided by the Russian bailiff's service in relation to an order from the court in Tyumen.

The company said there was no "legitimate basis" for the court case against BP or the raid. The legal entity searched in the raid - BP Exploration Operating Company Ltd - had “no connection to the Tyumen process,” the statement read. Let the games begin! Maybe this time Markey can be the referee!

© Gaurav Sharma 2011. Photo: ExxonMobil office exterior, Houston, Texas, USA © Gaurav Sharma, March 2011

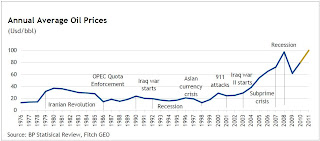

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)